What if saving for an emergency was easier when your income jumps from $1,200 one month to $5,800 the next?

You shouldn’t try to save like a salaried person when your pay swings that much.

You need a simple system that bends with variable cash flow, locks in progress every time money arrives, and keeps taxes and bills from eating your cushion.

This post gives clear, step-by-step moves, percentage rules, separate accounts, a smoothing buffer, and automation, so you can build a six-to-twelve month fund without waiting for a “good” month.

Immediate Steps to Start Building an Emergency Fund with Irregular Self-Employment Income

When your income swings between $1,200 one month and $5,800 the next, a traditional “save 10% every paycheck” plan falls apart fast. Self-employed workers need a system that bends with variable cash flow but still locks in consistent progress toward a cushion that covers rent, insurance, and groceries when clients disappear or invoices pay late.

The zero-sum budget solves this by living off last month’s income and assigning every dollar a job before the new month starts. You know what you earned in March, so in April you allocate that exact amount to rent, utilities, insurance, subscriptions, debt payments, taxes, and savings. If March was lean, you trim nonessentials in April. If March was flush, you push the surplus straight into your emergency fund or tax account instead of inflating your lifestyle. The 45% paycheck allocation rule layers on top: every time money lands in your account, you immediately route 30% to taxes, 5% to business reinvestment, and 10% to emergency savings. The remaining 55% covers living expenses or gets reinvested if the business needs it. In a $700 week, that’s $70 to your emergency fund. In a $300 week, you still move $30. Over six months, those uneven contributions add up to real months of coverage.

Practical first steps to start today:

- Assign every dollar a job using last month’s actual income as your spending ceiling for this month.

- Set a fixed percentage rule (start with 10% of every deposit to emergency savings, even if the deposit is small).

- Open a separate high-yield savings account labeled “Emergency Fund” so the money isn’t sitting with your operating cash.

- Calculate your bare-minimum monthly costs (rent, insurance, utilities, phone, groceries) to know what one month of coverage actually looks like.

- Schedule a recurring transfer on the day after your typical large client payment lands, automating at least part of the 10% rule.

Even a $30 contribution in a tough month keeps the habit alive and adds up faster than waiting for a “good” month to save a lump sum.

Determining the Right Emergency Fund Amount for Self-Employed Workers

Self-employed workers should target six to twelve months of essential living expenses, not three like a salaried employee. When your income can drop to zero for an entire quarter if a big contract ends, a short runway leaves you one surprise car repair away from credit-card debt. Start by adding up fixed monthly costs: rent or mortgage, utilities, minimum loan payments, insurance premiums (health, car, liability), cell phone, internet, transportation, groceries, and household basics. If that total is $3,000, a six-month fund is $18,000 and a twelve-month fund is $36,000.

Use one of three calculation methods depending on how conservative you want to be. The 12-month rolling average of your net income and expenses smooths out seasonal swings and gives you a realistic middle-ground number. The lowest-three-months method takes your three leanest months in the past year, averages them, and uses that as your monthly target. It’s pessimistic but safe if your work is highly seasonal. The fixed-essential-expenses method ignores income entirely and just lists what you must pay every month no matter what, giving you a floor to aim for first. Whichever you pick, separate personal living expenses from business operating costs. If you also need to cover $2,000 a month in business fixed expenses (software, rent, contractor fees), build a parallel three to six month business reserve in addition to your personal emergency fund.

| Expense Category | Amount | Notes |

|---|---|---|

| Rent/Mortgage + Utilities | $1,400 | Fixed housing and basic services |

| Groceries, Phone, Internet | $600 | Food, communication essentials |

| Insurance (Health, Car, Liability) | $550 | Premiums that cannot be skipped |

| Minimum Debt Payments | $300 | Student loan, car loan minimums |

| Transportation (Gas, Maintenance) | $150 | Bare-minimum to stay mobile |

| Total Monthly Baseline | $3,000 | 6 months = $18,000; 12 months = $36,000 |

Budgeting Methods That Work for Variable or Seasonal Income

The baseline-pay method stabilizes your life by creating an artificial paycheck even when revenue swings wildly. You calculate a conservative monthly income figure (either your 12-month trailing average or the median of your last year’s earnings) and pay yourself that exact amount from your business account into a personal checking account every month. Surplus months build up a buffer in the business account (one to three months of that baseline amount), and lean months draw from the buffer instead of forcing you to cut groceries or skip a credit-card payment. This smoothing account acts like an internal employer, absorbing the shocks so your household budget stays predictable. “I pay myself $3,200 on the first of every month, whether I invoiced $1,800 or $7,500 last month. The rest either sits in the buffer or funds my emergency and tax accounts.”

Zero-based budgeting adapts to fluctuating income by treating each month as a unique financial event. At the start of the month, you allocate last month’s actual net income to categories until you hit zero dollars unassigned. If you earned $4,200 in April, you assign $4,200 in May across all buckets (rent, food, savings, taxes) and stop. If you only earned $2,500, you fund essentials first, pause discretionary spending, and pull from your smoothing buffer if needed. The discipline is in the assignment step: every dollar gets a job before the month starts, so you’re never guessing mid-month whether you can afford something.

Percentage-based methods work well for people who dislike rigid category limits. You set rules like “30% of every deposit to taxes, 15% to emergency savings, 10% to business costs, 45% to living expenses.” When a $5,000 invoice clears, $1,500 goes to taxes, $750 to emergency savings, $500 to business expenses, and $2,250 to your personal account. When a $1,200 payment arrives, the same percentages apply but the dollar amounts shrink proportionally. This approach requires less monthly planning than zero-based budgeting but demands strict adherence to the percentage rules, especially in high-income months when it’s tempting to spend the windfall instead of banking it.

Separating Business, Personal, Tax, and Emergency Accounts for Better Cash Control

Mixing business revenue and personal spending in one checking account is how freelancers accidentally spend their tax money on a vacation and then panic in April. A clean four to five account structure removes that risk and automates good behavior. Start with a business checking account where all client payments land. From there, money flows into dedicated buckets: a tax account that holds 25 to 30% of gross income for federal, state, and self-employment taxes; a personal checking account that receives your fixed monthly “paycheck” transfer; a buffer or smoothing account that stores one to three months of baseline income to cover timing gaps; and a high-yield savings account labeled “Emergency Fund” that you only touch in a true crisis.

When you separate accounts, the decision about where money should go happens once (when you set up the automatic transfer rules) instead of every time you look at your balance and wonder if you can afford something. Your tax account grows quietly in the background, covering quarterly estimated payments without drama. Your emergency fund becomes invisible, making it psychologically harder to raid for a non-emergency. Your personal account only holds money you’re actually allowed to spend, which eliminates the cognitive load of calculating “how much of this $8,000 balance is really mine?”

Set up your account flow in this order:

- Business checking receives all client payments and pays all business expenses (software, contractors, supplies).

- Tax holding account receives 25 to 30% of every deposit the same day the money lands. Treat this like a bill you pay to the IRS in advance.

- Emergency savings (HYSA) receives 10 to 30% of each deposit until you hit your six to twelve month target.

- Buffer/smoothing account holds surplus from high-income months; you draw your fixed monthly transfer from here into your personal account, keeping your household budget stable even when business revenue is choppy.

Automating Savings and Setting Percentage-Based Rules for Each Payment

Relying on willpower to move money into savings after every invoice is a plan that works twice and then fails when you’re tired or distracted. Automation removes the decision and locks in progress whether you’re paying attention or not. Set up per-invoice rules the day you connect your payment processor or bank: 25 to 30% of every deposit goes immediately to your tax account, 10 to 30% goes to your emergency fund, and the remainder hits your operating or personal account. Most business checking accounts and apps like QuickBooks Self-Employed or FreshBooks let you create automatic transfer rules triggered by incoming payments, or you can schedule weekly transfers if your income arrives in unpredictable chunks.

Round-up rules and micro-savings apps add small but steady contributions on top of your percentage rules. Apps like Qapital or features in banks like Chime automatically round every debit transaction to the nearest dollar and move the difference into savings. $3.67 coffee becomes $4.00, and $0.33 goes to your emergency fund. Over a month of normal spending, that might add $20 to $40 without you noticing. Stack that with a 15% per-invoice rule and you’re building the fund from two directions at once.

Frequency and timing matter as much as the percentages. If most of your income lands mid-month, schedule your automatic transfer for the 16th. If you get paid irregularly, set a weekly transfer of a small fixed amount ($50 to $100) to keep momentum going between big invoices. The psychological win of seeing the balance grow every week reinforces the habit, even if the dollar amounts vary.

- Per-invoice rule example: Client pays $3,000, $900 (30%) to tax account, $450 (15%) to emergency fund, $1,650 to operating account, all automatic within 24 hours.

- Weekly fixed transfer: Every Friday, move $75 from business checking to emergency HYSA regardless of that week’s income.

- Round-up savings: Enable round-up on business debit card; at month-end, app sweeps accumulated spare change (usually $30 to $60) into emergency fund.

- Surplus sweep rule: If business checking balance exceeds $8,000 at month-end, automatically transfer the surplus above $5,000 into your buffer or emergency account.

Income Smoothing and Cash-Flow Protection Tactics for Freelancers and Contractors

Shortening the time between “work completed” and “money in account” is one of the fastest ways to smooth cash flow and make saving easier. Standard Net-30 or Net-60 invoice terms stretch your cash thin and create artificial lean months even when you’re busy. Switch to Net-7 or Net-15 terms, and suddenly the revenue from this week’s work arrives before next week’s rent is due. Add a 2% discount for clients who pay within five days (“2/5 Net 15” in invoice language) and you’ll see 30 to 50% of clients pay early to grab the savings, which pulls cash forward and reduces the need to dip into your buffer.

Requiring deposits upfront (20 to 50% of project cost) before starting work creates an instant cash injection and reduces the risk of non-payment. A $6,000 project with a 30% deposit puts $1,800 in your account on day one, covering part of your monthly expenses before you’ve done the work. The remainder comes due on delivery, cutting the payment gap in half compared to billing everything at the end. This tactic is standard in creative services, consulting, and construction; clients expect it, and it protects both sides by demonstrating commitment.

Retainer agreements turn unpredictable project income into predictable monthly revenue. A client who normally hires you for three $2,500 projects per year might agree to a $500/month retainer for ongoing access to your work, guaranteeing you $6,000 annual revenue spread evenly instead of three lumpy payments. Even one or two retainer clients create a baseline income floor that covers essential expenses, letting you treat project work as surplus that accelerates your emergency fund.

- Shorten payment terms from Net-30 to Net-7 or Net-15, and offer a small early-payment discount to pull cash forward by two to three weeks.

- Require 20 to 50% deposits on all projects over $1,000 to create immediate cash flow and reduce non-payment risk.

- Negotiate retainer contracts with repeat clients to convert project work into steady monthly income, even if the retainer is smaller than the project rate.

Cutting Personal and Business Expenses to Accelerate Emergency Savings

Trimming 10 to 20% of discretionary spending frees up $200 to $800 per month for most self-employed households, cutting your emergency-fund timeline nearly in half without requiring you to earn more. Start with subscriptions and recurring charges. Software you forgot you’re paying for, streaming services you opened once last year, memberships you don’t use. A quick audit usually reveals $50 to $150 in monthly charges that can be paused or canceled immediately. On the business side, renegotiate SaaS tools to annual plans (often 15 to 20% cheaper than monthly) or downgrade to lower tiers if you’re not using premium features.

Temporarily reducing owner draws during the fund-building phase is the self-employed equivalent of a salaried worker’s aggressive savings sprint. If you normally pay yourself $4,000 a month and your bare-minimum expenses are $2,800, drop your draw to $3,200 for six months and route the $800 difference directly into your emergency fund. It’s not comfortable, but it’s short-term, and it can turn a 24-month savings timeline into a 12-month sprint. The key is setting a specific end date (“I’m doing this until I hit $15,000 in the fund”) so it doesn’t feel permanent.

- Cancel unused subscriptions: audit recurring charges and cut $50 to $150/month in forgotten software, streaming, or membership fees.

- Switch to annual billing for essential tools to save 15 to 20% compared to monthly plans.

- Pause discretionary business spending: delay equipment upgrades, conference travel, or non-essential marketing for 6 to 12 months and redirect that cash to savings.

- Reduce dining out and convenience spending by 30 to 50% during the build phase; meal prep and home coffee can free $150 to $300/month.

- Temporarily lower owner draws by $500 to $1,000/month and route the difference straight to your emergency fund until you hit your target.

Where to Store Your Emergency Fund for Maximum Safety and Liquidity

Your emergency fund needs to be boring, safe, and available the day your car breaks down or a client disappears. That rules out stocks, crypto, and anything that could drop 20% the week you need it. High-yield savings accounts (HYSA) hit the sweet spot: FDIC-insured up to $250,000, instant access by transfer (usually same-day or next-day), and yields around 3 to 5% APY as of 2024, which is 10 to 15 times better than a traditional savings account paying 0.30%. Online banks like Ally, Marcus, and Capital One 360 consistently offer top-tier rates because they don’t operate physical branches, and your money is just as safe as it would be at a big-name bank.

For funds beyond your first three to six months of expenses, a CD ladder or short-term Treasury bills can capture slightly higher yields without locking your money away for years. A CD ladder works like this: split $12,000 across four 3-month CDs of $3,000 each, staggered so one matures every month. You earn a higher rate than a savings account (often 0.25 to 0.75% more), and every 90 days a chunk becomes liquid again if you need it. Treasury bills (T-bills) with 4-week, 8-week, or 13-week maturities offer similar yields and are backed directly by the U.S. government, with zero state income tax on the interest. Both strategies keep the bulk of your fund accessible within a quarter while earning a bit more than plain HYSA.

Keep your first $500 to $1,000 in a regular checking account for true same-day emergencies (flat tire, urgent medication, last-minute flight). The next three to six months goes into a high-yield savings account for instant access with better returns. Anything beyond six months can sit in a CD ladder or T-bills if you want to squeeze out extra yield, but only if you’re confident you won’t need that tier immediately. Most self-employed workers stop at HYSA because liquidity beats an extra 0.5% when your income is unpredictable.

| Account Type | Liquidity | Typical APY (2024) | Best Use Case |

|---|---|---|---|

| Checking (Immediate Buffer) | Same-day | 0 to 0.50% | $500 to $1,000 for instant emergencies |

| High-Yield Savings (HYSA) | 1 to 2 business days | 3.00 to 5.00% | Core fund: 3 to 6 months of expenses |

| Short-Term CDs (3 to 12 month) | Locked until maturity | 4.00 to 5.50% | Extended reserve if laddered |

| Treasury Bills (4 to 26 week) | Can sell early, slight loss | 4.50 to 5.25% | Extended reserve, no state tax |

When and How to Use Your Emergency Fund (and How to Rebuild It)

An emergency fund is for emergencies, not “I really want this” purchases. The definition of an emergency is simple: an unexpected expense or income loss that you cannot cover with your normal cash flow and that will cause serious harm if ignored. Medical bills, urgent home or car repairs, loss of a major client that drops your income below survival level, or a family crisis that requires immediate travel all qualify. A great deal on new camera gear, a vacation because you’re burned out, or covering regular expenses after you overspent last month do not.

If you do need to tap the fund, take only what you need and create a replenishment plan the same week. Decide whether you’ll rebuild in three months, six months, or twelve months depending on how much you withdrew, and calculate the monthly contribution required to hit that deadline. If you pulled $4,000 and want it back in six months, you need to save roughly $670 per month on top of your normal expenses. Temporarily increase your savings percentage from 10% to 25 to 40% of income, cut discretionary spending by another 10 to 20%, and pause non-essential business investments until the fund is whole again. Treat rebuilding with the same intensity you used to build it the first time, because the fund only works if it’s there for the next shock.

The worst time to use your emergency fund is when a lower-cost option exists. If your income dips but you can cover expenses by trimming subscriptions, delaying a purchase, or picking up a quick side gig, do that first. If a surprise expense can be negotiated into a payment plan with zero interest (medical bills, some contractors), that’s often better than draining savings in one hit. Your emergency fund is the last line of defense, not the first move.

- Define your personal emergency trigger: write down the specific scenarios that justify using the fund (income below $X, unexpected expense over $Y, health/family crisis).

- Withdraw only the amount you need: if the car repair is $1,200, don’t pull $2,000 “just in case.” Keep the rest working in your HYSA earning interest.

- Create a replenishment schedule immediately: calculate how many months to rebuild, set a temporary higher savings percentage (30 to 40%), and mark a calendar date when the fund should be restored.

Sample Savings Plans and Timelines for Different Types of Self-Employed Workers

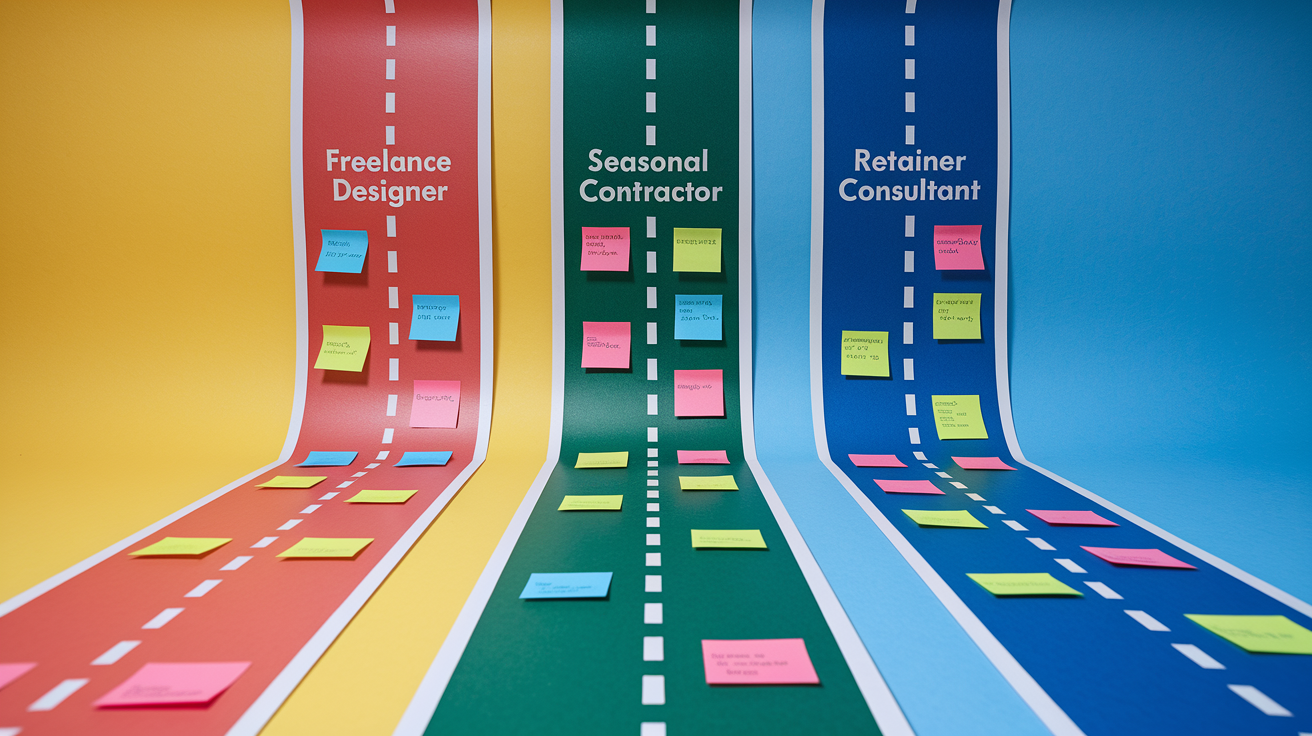

A freelance graphic designer earning between $2,000 and $6,000 per month, with an average of $3,500 and essential monthly expenses of $2,200, needs a six-month emergency fund of $13,200. If she saves 15% of her average gross income, that’s $525 per month, putting her on a 25-month timeline to full coverage. To accelerate, she adopts a variable savings rule: in any month where income exceeds $4,000, she saves 30 to 40% of the surplus above her $2,200 baseline instead of increasing spending. A $5,500 month means $3,300 surplus, and 35% of that ($1,155) goes straight to the fund. Three or four high months per year can cut the timeline to 15 to 18 months while keeping lean months manageable with smaller contributions.

A seasonal contractor in landscaping or event production faces dramatic swings: six busy months averaging $8,000+ per month and six slow months around $2,500, with personal expenses of $4,000 monthly. A twelve-month emergency fund of $48,000 feels impossible until he restructures the savings plan around his busy season. During the six high months, he saves 40 to 50% of gross income, banking $3,200 to $4,000 per month. That’s $19,200 to $24,000 in six months. During the slow season, he saves nothing and draws from the fund or his smoothing buffer to cover the shortfall. Over two cycles, he builds the full $48,000 fund while maintaining stable personal spending year-round. The key is resisting lifestyle inflation during flush months and treating the busy season as “fund the off-season” time, not “spend freely” time.

| Scenario | Monthly Expenses | Target Fund Size | Estimated Timeline |

|---|---|---|---|

| Freelance Designer $2k to $6k income, avg $3.5k |

$2,200 | $13,200 (6 months) | 15 to 25 months 15% base + 35% of surplus |

| Seasonal Contractor Busy $8k+, slow $2.5k |

$4,000 | $48,000 (12 months) | 12 to 18 months 40 to 50% savings in busy season |

| Consultant with Retainers Stable $5k base + project spikes |

$3,500 | $21,000 (6 months) | 10 to 14 months 20% of base + 50% of project income |

Tools, Apps, and Systems to Manage Irregular Income and Build Savings

YNAB (You Need A Budget) is built specifically for people whose income doesn’t arrive on a schedule. It forces zero-based budgeting by making you assign every dollar a job, handles month-to-month rollovers cleanly, and lets you prioritize categories when money is tight. The learning curve is real, but users with variable income report it’s the only budgeting app that doesn’t break when paychecks are uneven. Mint and Personal Capital work better for people who want passive tracking and net-worth dashboards without the hands-on budget assignment, though neither adapts as well to true income volatility.

For invoicing and bookkeeping, QuickBooks Self-Employed and FreshBooks both integrate income tracking with automatic mileage logs, expense categorization, and estimated quarterly tax calculations. Wave is free and handles invoicing, receipt scanning, and basic reporting, making it the best starting point if you’re not ready to pay $15 to $30 per month for software. All three can trigger automatic transfers or reminders when an invoice is paid, which ties directly into your per-invoice savings rules.

High-yield savings accounts from Ally, Marcus by Goldman Sachs, or Capital One 360 offer competitive APYs (usually within 0.10 to 0.25% of each other) and no monthly fees. Ally’s buckets feature lets you split one savings account into virtual sub-accounts for different goals (emergency fund, tax fund, vacation fund) without opening multiple accounts. Qapital and similar micro-savings apps add automation on top of your main accounts, letting you set rules like “round up every transaction” or “save $5 every time I skip coffee” to build the fund in the background.

- YNAB: best for hands-on zero-based budgeting with irregular income; handles month-to-month rollovers and priority spending when cash is tight.

- QuickBooks Self-Employed or FreshBooks: invoicing, expense tracking, mileage logs, and estimated quarterly tax calculations in one place.

- Wave: free invoicing and bookkeeping for bootstrapped freelancers; fewer features but solid for basic tracking and client billing.

- Ally, Marcus, or Capital One 360: high-yield savings with no fees, competitive APYs around 4 to 5%, and easy transfers; Ally’s buckets feature simplifies goal tracking.

- Qapital or Chime: micro-savings automation via round-ups, recurring rules, and percentage-of-deposit triggers; stacks on top of your main bank to add small contributions automatically.

Final Words

Start now: pick one rule and put it on autopilot—set a percentage from each invoice, open a dedicated emergency account, or schedule weekly transfers.

You’ve seen practical steps: zero-sum budgeting adapted for irregular pay, the 45% allocation to cover taxes/reinvestments/savings, income smoothing, and where to store funds.

If you still wonder how to build an emergency fund while self-employed, follow the milestones—small, steady deposits add up. You’ll be more secure sooner than you think.

FAQ

Q: What is the 3 6 9 rule for emergency fund?

A: The 3‑6‑9 rule for emergency funds recommends 3 months for steady jobs, 6 months for most households, and 9 months or more for self‑employed or variable income to cover income gaps.

Q: How much emergency fund for self-employed?

A: The emergency fund for self‑employed should be 6–12 months of essential expenses, using your lowest three‑month income or a 12‑month average as the baseline; pick 12 months if seasonal or uncertain.

Q: What is the 50 30 20 rule for self-employed people?

A: The 50/30/20 rule for self‑employed means 50% needs, 30% wants, 20% savings/debt, but you should first reserve estimated taxes and reinvestment—consider a 45% allocation (30% taxes, 5% reinvest, 10% emergency).

Q: What is the 70/30/10 rule money?

A: The 70/30/10 money split totals 110% and isn’t workable; you likely mean 70/20/10: 70% living, 20% savings/debt, 10% giving. For self‑employed, set aside taxes before splitting.

{kind=link}